At Tinker Capital, we believe capital should be a tool for progress, not just a measure of returns. Disciplined investing, long-term thinking, and thoughtful stewardship can help inform better decisions. Here, we share perspectives at the intersection of strategy, growth, and purpose designed to challenge conventional thinking and spark smarter decisions in an ever-evolving market.

![]() "It ain't what you don't know that gets you into trouble. It's what you know for sure that just ain't so." Mark Twain

"It ain't what you don't know that gets you into trouble. It's what you know for sure that just ain't so." Mark Twain

Clarity Creates Confidence

Financial decisions often feel overwhelming—not because they are impossible to understand, but because they are rarely organized in a clear and disciplined way. At Tinker Capital, we believe financial planning should reduce anxiety, not increase it.

This FAQ page is designed to provide thoughtful answers to important questions. Our goal is not simply to give advice, but to help you understand the principles behind sound financial decision-making.

Managing your finances does not require complexity—it requires structure.

It begins with perspective: learn to want what you have more than wanting what you don’t. Financial satisfaction often comes from organization and intention, not constant accumulation.

At Tinker Capital, we use the R-E-T-I-R-E framework to simplify the process:

Risk Management – Identify, avoid, reduce, transfer, or retain risk appropriately.

Essentials of Cash Management – Establish sustainable budgeting and liquidity.

Tax Management – Improve after-tax outcomes over time.

Investment Management – Align investments with long-term goals and tolerance for volatility.

Retirement Planning – Focus on generating sustainable income throughout retirement.

Estate Planning – Ensure assets are transferred efficiently and intentionally.

When these elements work together, financial decisions become clearer and more purposeful.

The best time to invest is when you are prepared to remain invested during difficult markets.

There will always be headlines that suggest caution. Markets move through cycles of fear and optimism. However, long-term investors are rewarded not for predicting short-term movements, but for maintaining discipline.

Time in the market is far more powerful than attempting to time the market.

Losses are mathematically more damaging than gains are helpful.

A 20% loss requires a 25% gain to recover.

A 30% loss requires a 42.9% gain.

A 50% loss requires a 100% gain.

This asymmetry is why risk management is foundational to investment success. Avoiding large drawdowns protects the compounding process that builds wealth over time.

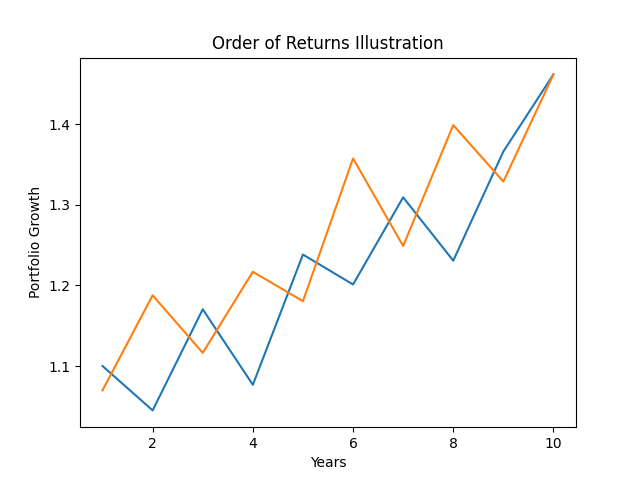

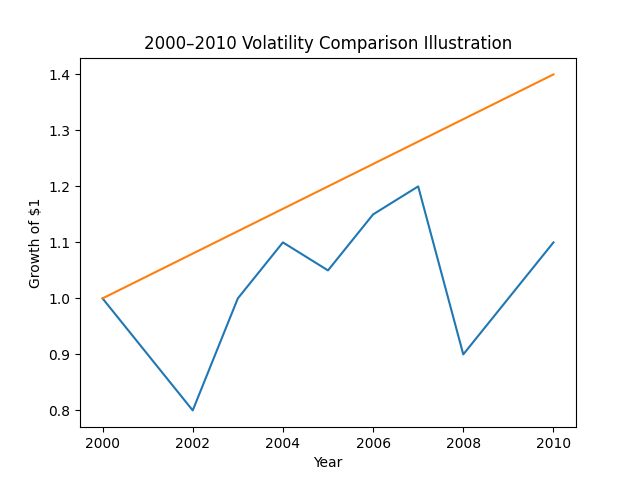

Uncertainty is a permanent feature of investing.

While moving to cash may feel safer in the moment, it often interrupts the compounding process. Market recoveries frequently occur before investors feel comfortable re-entering.

The order of returns may vary, but long-term outcomes tend to reward disciplined investors who remain invested.

Yes. Saving is not just about the dollar amount—it is about behavior.

If you save a small percentage of your income early in life, you establish a habit that scales as your income grows. Financial independence is built through consistent action over time, not occasional large efforts.

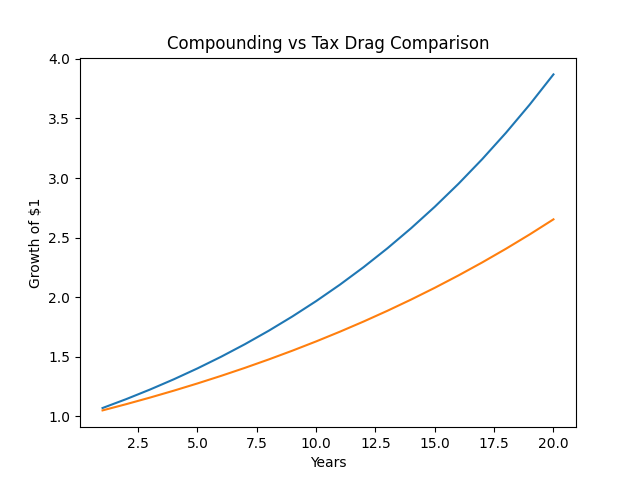

Retirement accounts provide structural advantages that enhance long-term growth.

They offer tax-deferred or tax-free growth, allow compounding to work efficiently, and may include employer contributions.

Over decades, the difference between taxed and tax-advantaged growth can be substantial.

Financial planning should first secure your independence before optimizing for legacy.

While tax efficiency for heirs is important, your retirement years may span decades. Ensuring sufficient income, flexibility, and protection should be the primary focus.

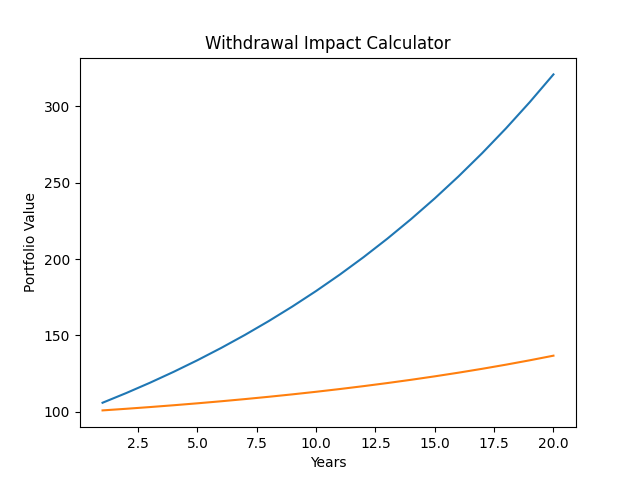

Withdrawals require strategy, particularly during volatile markets.

Selling assets during significant declines can lock in losses and increase the percentage required to recover. Maintaining lower-volatility assets to fund short-term needs helps protect long-term growth assets.

You may benefit from working with an advisor when financial decisions become complex, time-consuming, or emotionally challenging.

A disciplined advisor provides structure, perspective, and accountability—helping you remain aligned with long-term goals.

At Tinker Capital, relationships are central to our philosophy. You work directly with the advisor who understands your goals and financial circumstances.

The guaranteed enrollment period is critical. During this window, you cannot be denied coverage for pre-existing conditions.

Delaying decisions may limit future options. Careful evaluation upfront can prevent costly restrictions later.

We work best with individuals and families who value education, structure, and long-term planning over short-term speculation.

Our philosophy goes beyond managing dollars. We focus on helping you build personal capital. We believe true wealth is not just measured by portfolio size, but by the peace of mind, clarity, and confidence you feel in your financial life. Every investment decision we make is designed to support your ability to live an enriching, well-aligned life.

We integrate financial planning and investment management within a repeatable framework. Education and transparency are foundational to every client relationship.

Begin with a no-cost, no-obligation conversation with a financial professional at Tinker Capital. We discuss your goals, evaluate your current structure, and determine whether there is a strong mutual fit.

Most clients are referred by existing relationships or professional connections. We grow through trust and consistent results.

Too often, we enjoy the comfort of opinion without the discomfort of thought.

John F. Kennedy